How to Read and Understand a Credit Report

At first look, the information on your credit report may appear to be challenging to read and understand. Knowing how to read your credit report and what corporations have reported to your history is essential.

Experian, TransUnion, and Equifax are the three major credit reporting agencies, and the credit reports created for you by these companies are laid out the same way.

Credit Report Sections and Codes

There are 11 sections to a credit report with only a few minor differences.

You want to review all three because each company may gather different information, and specific lenders may only report to one or more bureaus. This may cause you to score higher on one report than the other.

I’ve listed them individually, describing each section. Although they may appear in different places on your report, I’ve listed them in the order in which they are most likely to occur.

Did You Know?

- Before applying for a car loan, familiarize yourself with how a car dealership’s finance process works and the correct way to finance a car so you will not overpay on excessive interest rate charges or bank fees.

- You should always request and review your credit reports and scores before applying for any loan. You put yourself at a disadvantage when the lender knows more about what’s been reported to your credit bureaus than you do.

Credit Report Heading

The heading of a credit report is normally found at the very top and right of the report. It will contain the Credit Bureau’s information, the Companies name, address, phone number, and the date the credit report was pulled.

Personal and Identifiable Information

This section of the credit report is your personal information. It includes your name, social security number, date of birth, phone number (if available), and up to three different addresses.

Your most recent address appears directly below your name, with your previous addresses appearing below your name in chronological order. Your employment and birth date information will appear to the right of your addresses and above the summary score.

This information is only available if inputted when you apply for credit.

Employment Information and Past History

This section of the credit report will contain your employment history and information.

If available, this may include the company name, occupation, income, hire date, and release date.

This information, along with personal information, gets reported on your credit report by an individual inputting the information when you apply for credit.

Public Records Reported to a Credit Bureau

This section of your credit report will show if there are any civil actions with dollar amounts awarded. They usually appear towards the top of your credit report below the score summary in an area named Public Records. This information includes liens, civil actions against you, foreclosures, and bankruptcies.

The public records section also includes the account’s name and number, filing date with the court, and status date. Whether the status is released, vacated, satisfied, dismissed, or discharged, type and amount of public record, docket or certificate number, and code describing your relationship to the public record item, as required by the Equal Credit Opportunity Act. The plaintiff’s name, asset amounts, liability for bankruptcies, and voluntary indicator for bankruptcies also.

Descriptions for the above chart:

Credit Report Score or Score Card Section

There are many names for the number score on your credit bureau, FICO, Beacon, Beacon Score, Bureau Score, or Empirica, to name a few. It is generally located above your trade and credit information and is the overall rating of your credit history. There are up to 4 factors disclosed and are displayed based on their impact on the final score.

- Typically scores above 625 are worthy of loans from banks.

- Scores range from the low 400’s to the highs of 850.

- Scores over 800 are seldom seen; these individuals have excellent credit, and most qualify for special low-interest rates and programs.

- Scores above 700 are considered very good. Most qualify for special rates and terms without any added documentation.

- The most common scores range between 600 and 700, and most are considered very good; depending on the depth of your credit, you may have to provide extra documentation to be approved for a loan. You may or may not fall into the most exclusive car buyer’s rates, but you will likely not have to pay the sub-prime rates.

- Scores 600 and below are considered risky or sub-prime and will warrant further proof and documentation to be qualified for a loan. You may have to pay much higher interest rates, put a larger down payment down, show proof of residence, proof of home phone, proof of income, and provide the lender with personal references.

- If you have no score or it is not available, it means that you have no credit history, and no one has ever inquired about your credit history. You can look at your report under your name and see if the “On File Since” is the same date as you inquired. If it’s the same, you’ve just created your credit file.

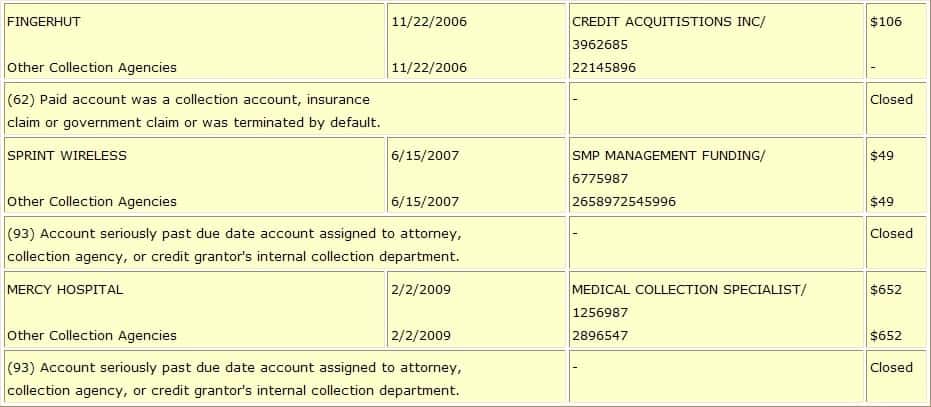

Collections Section

This section of your credit report will identify your accounts that have been sent to professional debt collecting firms. Collection information will include the name of the collection agency providing the data, the collector’s kind of business designators, and the collector’s account number for your account.

The date the original creditor charged off the amount. When the creditor verified the amount, the initial dollar amount of the collection, the balance owed as of the date closed or confirmed, the explanation of the current account status reported by the collection agency, and the original creditor’s name will all be included in this information.

Descriptions for the above chart:

Public Records Reported to a Credit Bureau

This section of your credit report will show if there are any civil actions with dollar amounts awarded; they usually appear towards the top of your credit report below the score summary in an area named Public Records. This information includes liens, civil actions against you, foreclosures, and bankruptcies.

The public records section also includes the account’s name and number, filing date with court, and status date.

If the status is released, vacated, satisfied, dismissed, or discharged, type and amount of public record, docket or certificate number, and code describing your association to the public record item per the Equal Credit Opportunity Act. The plaintiff’s name, asset amounts, liability for bankruptcies, and voluntary default indicator also.

Descriptions for the above chart:

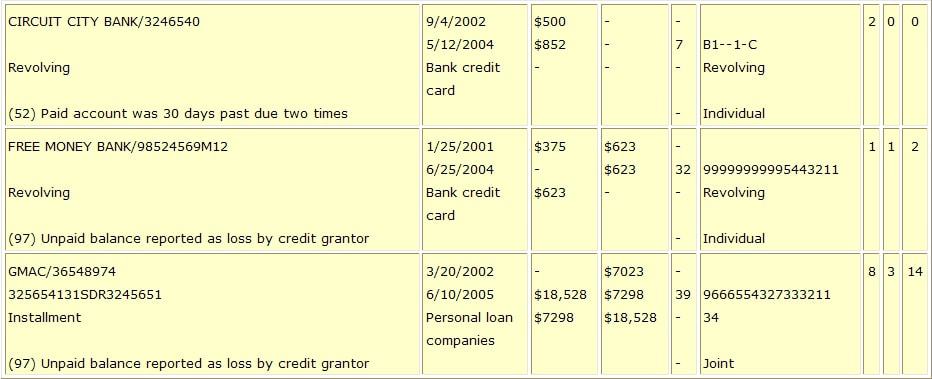

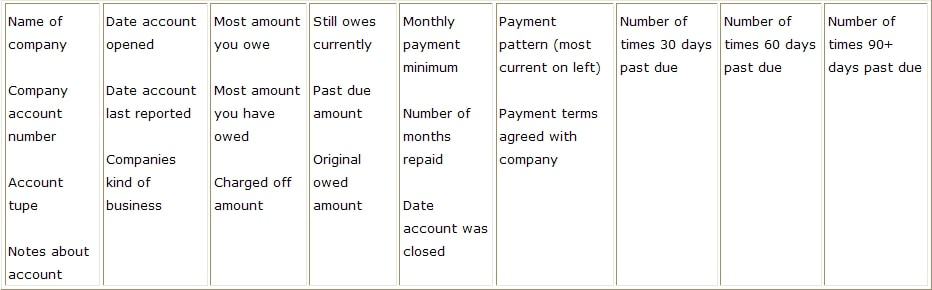

Trades or Tradeline Section of a Credit Report

The trades section of your credit report is where creditors report credit cards and loan amounts with their payment histories.

The creditor’s name is in the left column, the credit amount is in the center, and the payment history is in the right column.

This section provides a breakdown by month your payment history.

Descriptions for the trade line section of a credit bureau:

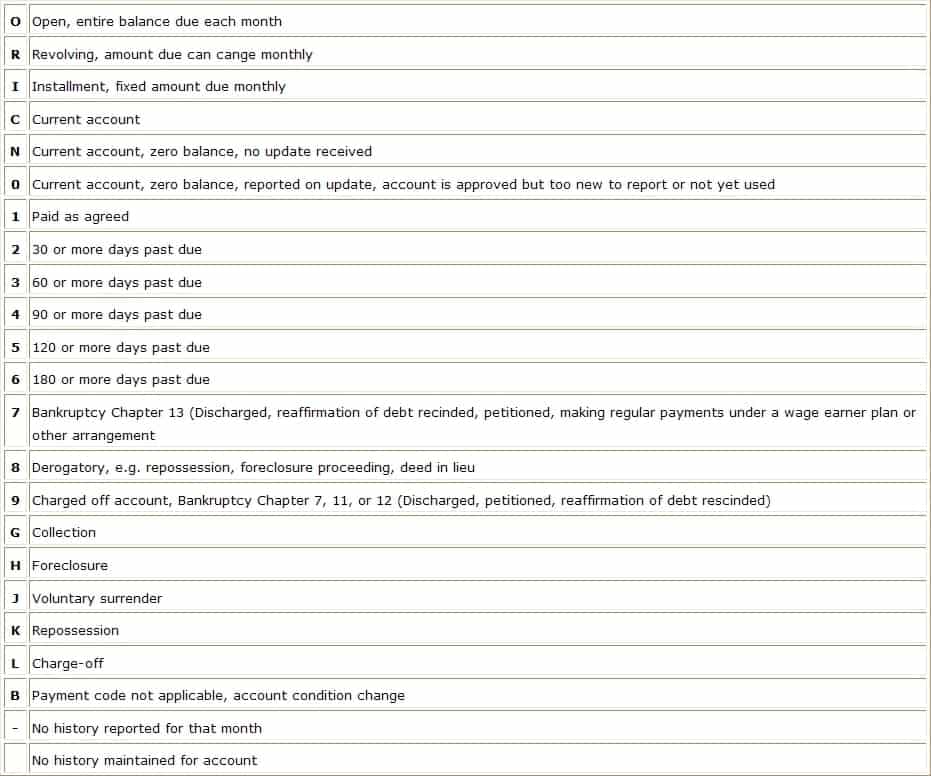

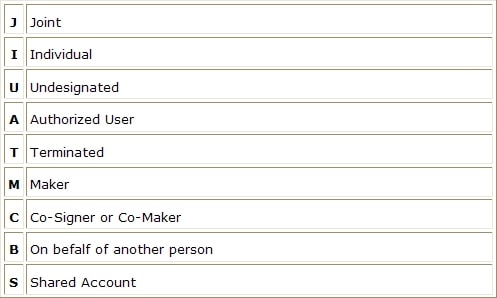

Payment History and Codes

On the far right-hand side of your credit report, you will generally find your payment history for the past 24 months. Codes reflect the monthly status of your accounts and are displayed for balance reporting loans.

There is no grading of charge-offs or collections. On different credit reports, some codes have various meanings. All of the other functions of each code are given below. The following are the codes’ definitions.

In addition to the codes described above, each account will have a letter indicating your connection to that account.

Using the above coding, you can go to the column on your credit report, and the following alphanumeric combinations would be reasonable indications that you have excellent credit history: 1, R1, I1, or O1.

You would not want to find or see these 2, 3, 4, 5, 6, 7, 8, or 9’s.

Did You Know?

Don’t let the car dealer know more about your credit history and score than you do. This puts you at a severe disadvantage and could cost you thousands of dollars.

Errors are commonly found in credit reports. You can quickly fix them, but you need to find them and correct them before sitting in a car dealership wanting to buy your dream car. Not fixing these errors beforehand will cost you money over the life of your next new or used car loan.

A credit report is like a report card for your financial well-being. It will list creditors you owe money to and your history on how you pay them back.

What can you find on your credit report?

- Your private information and history include name, aliases, address, previous addresses, social security number, birth date, and past and present employers.

- Your credit history includes who you owe money to, who you’ve paid and if you pay on time.

- Public records like tax liens, judgments, or bankruptcies.

- It will also show inquiries from people or companies that have recently pulled your credit report.

Payment History and Codes

On the far right-hand side of your credit report, you will generally find your payment history for the past 24 months. Codes reflect the monthly status of your accounts and are displayed for balance reporting loans.

There is no grading of charge-offs or collections. On different credit reports, some codes have various meanings. All of the other functions of each code are given below. The following are the codes’ definitions.

In addition to the codes described above, each account will have a letter indicating your connection to that account.

Using the above coding, you can go to the column on your credit report, and the following alphanumeric combinations would be reasonable indications that you have excellent credit history: 1, R1, I1, or O1.

You would not want to find or see these 2, 3, 4, 5, 6, 7, 8, or 9’s.

Credit Report Inquiries

This part of your credit report is a list of the companies that have inquired about your credit history, usually to extend new or additional credit to you. Numerous inquiries will lower your score by about 2 points per inquiry.

Description of the above chart:

![]()

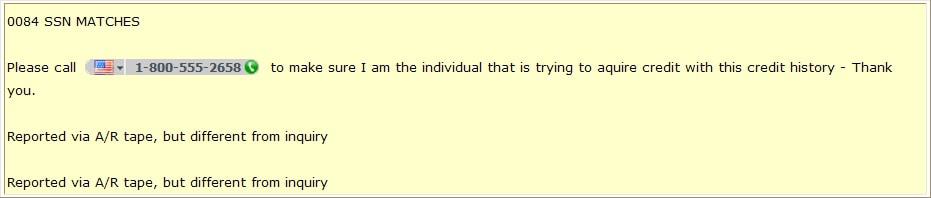

Warnings and Messages section of a Credit Bureau

Your credit report’s warnings and messages section is usually the last section on the account. This section lists any messages that have to do about your credit, name, address, or social security number.

There may even be a personal message to call a number to verify that the person using your credit history is the actual person it belongs to.

About the author

My name is Carlton Wolf, and I’ve been in the car business since 1994, both retail and wholesale. I created the Auto Cheat Sheet to better educate buyers about the deceptive sales practices used by many dealerships throughout the country. Please understand that not all car dealers are dishonest. However, you never know who you’ll be dealing with, though. I’m willing to share my knowledge and experience with anyone who listens. Keep in mind that I’m a car guy, not a writer.

My name is Carlton Wolf, and I’ve been in the car business since 1994, both retail and wholesale. I created the Auto Cheat Sheet to better educate buyers about the deceptive sales practices used by many dealerships throughout the country. Please understand that not all car dealers are dishonest. However, you never know who you’ll be dealing with, though. I’m willing to share my knowledge and experience with anyone who listens. Keep in mind that I’m a car guy, not a writer.